An offset account is one of the most widely used features in Australian home lending, yet many borrowers either underuse it or misunderstand how it works. For investors and owner-occupiers weighing up loan structures, understanding the mechanics of an offset account can mean the difference between paying tens of thousands in additional interest or saving the same amount over the life of a loan.

How an offset account works

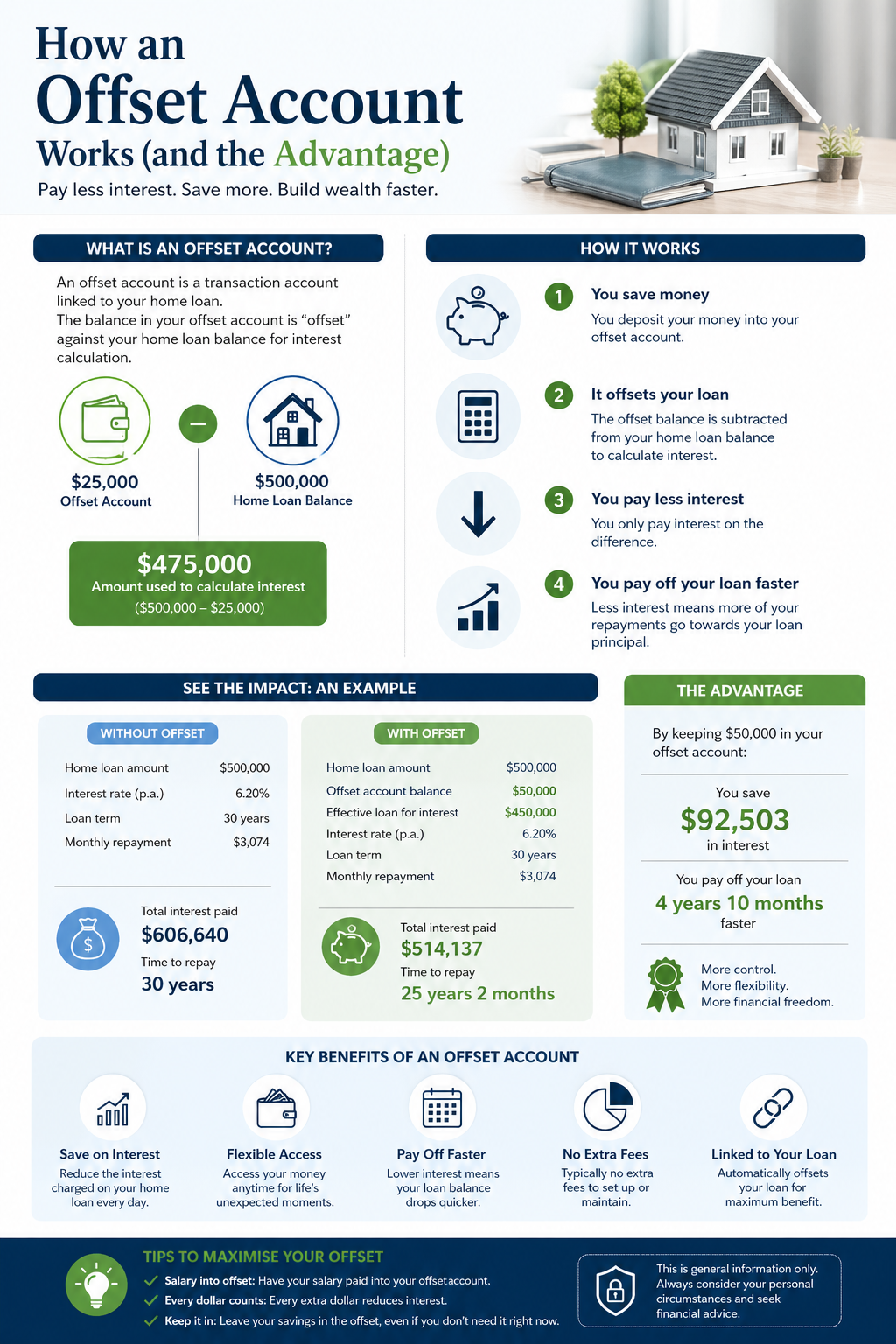

An offset account is a transaction account linked to a home loan. The balance held in the account is "offset" against the loan principal when interest is calculated. Borrowers are charged interest only on the net difference between the loan balance and the offset balance.

For example, a borrower with a $500,000 mortgage and $50,000 sitting in their offset account is charged interest on $450,000 rather than the full loan amount. The funds in the offset remain accessible at any time, functioning like a regular everyday account.

Unlike making direct repayments into the loan, money in an offset account is not committed. It can be withdrawn, spent, or moved without redraw fees or lender approval.

Offset versus redraw

Offset accounts are often confused with redraw facilities, but the two operate differently. A redraw facility allows borrowers to access extra repayments they have made on the loan. While the interest savings can be similar, redraw funds are technically part of the loan, not a separate account.

This distinction has tax implications for investors. Funds withdrawn from a redraw facility on an investment loan can affect the deductibility of interest, depending on how the money is used. Offset accounts, because they are separate transaction accounts, generally avoid this complication.

The Australian Taxation Office has long treated redraws as new borrowings for tax purposes. For property investors, this is a critical structural consideration.

When an offset account makes sense

The financial benefit of an offset account depends on how much money sits in it and for how long. Borrowers who maintain consistent balances, including salary deposits, savings buffers, or rental income, typically extract the most value.

Owner-occupiers with surplus cash flow often use offset accounts to reduce non-deductible interest while keeping funds liquid for emergencies or future purchases.

Property investors frequently use offset accounts attached to their owner-occupier loan, where interest is not tax-deductible. Reducing non-deductible interest first is generally more tax-efficient than reducing deductible interest on an investment loan.

When it may not be worthwhile

Offset accounts are not free. Many lenders charge higher interest rates or annual package fees for loans with offset features. For borrowers who keep only small balances in the account, the savings may not justify the additional cost.

Basic loan products without offset features often carry lower headline rates. A borrower with limited savings may be better served by a no-frills loan and a competitive rate than by paying a premium for an offset they barely use.

Some lenders also offer partial offset accounts, where only a portion of the balance is offset against the loan. These products typically cost less but deliver smaller savings.

The interest savings in practice

The mathematics of an offset account is straightforward. Every dollar held in offset reduces the interest charged at the loan's variable rate. On a $600,000 loan at 6 per cent, holding $30,000 in offset saves approximately $1,800 in interest in the first year alone, with the compounding effect growing over time as the loan balance reduces faster.

For borrowers maintaining higher balances, the savings can be substantial. A $100,000 offset balance on the same loan would save around $6,000 annually at current rates.

Considerations before opening one

Before choosing a loan with an offset account, borrowers should compare the total cost of the loan, including any rate premium and fees, against the realistic balance they expect to hold. Mortgage brokers and financial advisers can model different scenarios based on individual cash flow patterns.

Loan structure also matters. Offset accounts are typically available with variable-rate loans, though some lenders now offer them on fixed-rate products with limitations. Borrowers locking in a fixed rate should check whether their offset will function fully during the fixed period.

For investors building a portfolio, the choice of which loan to attach an offset to can have long-term tax and cash flow implications, and is generally worth discussing with an accountant before settlement.