On a typical Saturday morning in Sydney, Melbourne, or Brisbane, the housing market rarely looks political on the surface. At a suburban auction, it’s about budgets, borrowing power, and timing — not party ideology.

But behind the bidding paddles, Australia’s housing market is increasingly shaped by political choices made in Canberra and state parliaments. Property investment has become one of the most contested policy areas in the country, with Labor and the Coalition offering different approaches to the same underlying crisis: housing affordability.

While both sides agree Australia needs more homes, they differ on how to get there — and, crucially, how property investors should fit into the solution.

A shared problem, but different policy instincts

There is broad political agreement that Australia faces a structural housing shortage, particularly in major cities where population growth, migration, and limited housing supply have placed sustained pressure on prices and rents.

Where Labor and the Coalition diverge is not in diagnosis, but in emphasis.

The Coalition generally places stronger weight on supply-side solutions — such as faster planning approvals, reduced regulatory barriers for developers, and incentives designed to encourage private sector construction activity.

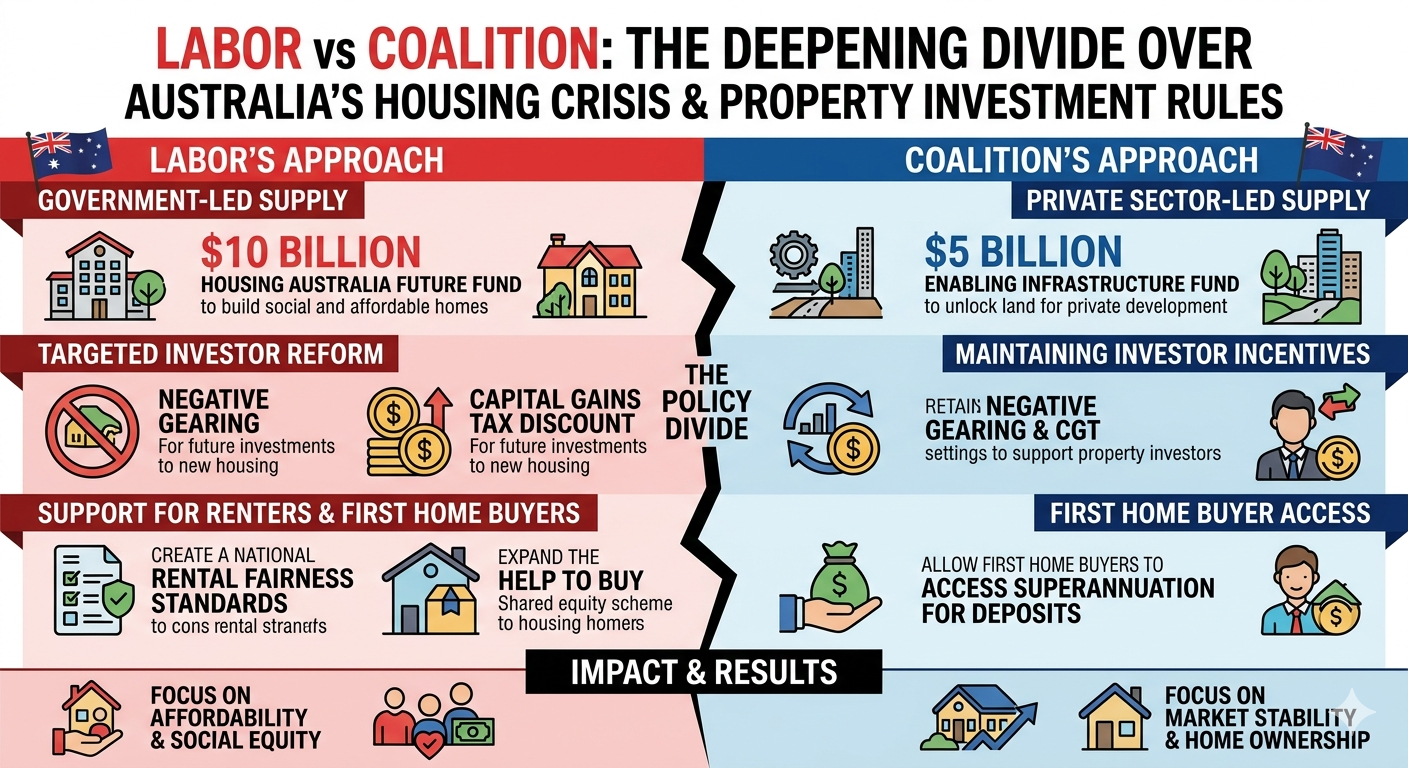

Labor, by contrast, places greater emphasis on a broader mix of interventions, including government-led housing investment, planning reform in coordination with states, and targeted support for first-home buyers and rental market stability.

Both approaches aim to increase housing supply, but they differ in the mechanisms used to achieve it and the role of government in shaping outcomes.

Negative gearing and tax settings: the enduring fault line

One of the most politically sensitive areas in Australian housing policy remains the tax treatment of property investment, particularly negative gearing and the capital gains tax (CGT) discount.

These settings allow property investors to offset rental losses against other income and reduce tax on capital gains when selling investment properties. They have been part of Australia’s tax system for decades and remain unchanged at a federal level.

The Coalition has consistently supported maintaining these settings, arguing they encourage investment in rental housing and support overall housing supply. This position is grounded in the view that private investors play a central role in providing rental accommodation across Australia.

Labor’s position is more nuanced. While the current federal Labor government has not pursued changes to negative gearing or the CGT discount, parts of the party — particularly in earlier policy debates — have supported reform options, often framed around improving housing affordability and reducing pressure on established housing markets.

At present, neither major party has implemented major changes to these tax settings. However, they remain a recurring subject in public debate and policy discussion, particularly during periods of housing stress.

First-home buyers and investors: competing priorities

A key difference between Labor and the Coalition lies in how each frames the balance between first-home buyers and investors.

The Coalition has typically focused on improving market access and supply conditions, with policies aimed at helping buyers enter the market through financial assistance measures and by supporting private sector development.

Labor has placed relatively more emphasis on affordability pressures and market access challenges, including expanded first-home buyer support programs and increased government involvement in housing supply initiatives.

Importantly, both parties acknowledge the importance of first-home buyers and investors in the system. The distinction lies in how they interpret market tension: whether it is primarily a supply problem, or also a distribution and access issue.

State governments are already reshaping investor conditions

While federal policy debates attract attention, state governments — many of them Labor-led — have already introduced changes that affect property investors more directly.

Across different jurisdictions, investors face varying combinations of stamp duty, land tax thresholds, and surcharges that differ from those applied to owner-occupiers. Some states have also introduced vacancy-related charges aimed at discouraging properties from remaining unoccupied in tight rental markets.

In Victoria, land tax settings and additional investment property surcharges have increased holding costs for some investors. In New South Wales, ongoing discussions around stamp duty reform and potential transitions toward land tax-based models continue to create uncertainty for long-term investment planning.

These differences are contributing to a more fragmented national market, where investment decisions are increasingly influenced by state-level policy environments rather than purely local price trends.

Foreign investment and build-to-rent: cautious convergence

Foreign investment in Australian residential property remains tightly regulated, particularly in relation to established housing stock. Most foreign investment is directed toward new developments, subject to approval processes and additional fees in some cases.

At the same time, both Labor and Coalition governments have shown support for increasing institutional investment in rental housing, particularly through build-to-rent developments.

These projects — typically large-scale apartment complexes designed specifically for long-term renting — are seen by policymakers as one way to increase rental supply and improve housing stability.

However, there is ongoing debate about how incentives should be structured, and whether institutional investors should receive different tax treatment compared to individual property investors.

Investor behaviour is already adjusting

Even without major legislative reform, investor behaviour is responding to the current policy and economic environment.

Higher interest rates compared to the ultra-low period of the early 2020s have reduced borrowing capacity and shifted investment strategies. Lenders have also maintained stricter serviceability assessments, which has affected the scale and composition of investor lending.

As a result, investors are increasingly focusing on rental yield and cash flow rather than relying primarily on capital growth. This shift is particularly evident in markets with stronger rental demand and tighter vacancy conditions.

Geographically, investment activity has become more diversified. While Sydney and Melbourne remain key markets, there is growing interest in secondary cities and outer metropolitan areas where entry prices are lower and yields are comparatively stronger.

The growing role of policy risk

An increasingly important factor in property investment decisions is policy risk — the possibility that taxation, regulation, or housing policy settings could change over time.

Unlike interest rates or market cycles, policy risk is harder to quantify but is increasingly considered by investors when assessing long-term returns.

This has encouraged more cautious and diversified investment strategies, including spreading portfolios across different states or prioritising markets perceived to have more stable regulatory environments.

In practice, this means housing investment decisions are no longer driven solely by price and rental performance, but also by expectations about future policy stability.

Where the political divide leads next

Australia’s housing market is unlikely to be reshaped by a single sweeping reform. Instead, it continues to evolve through incremental changes at both federal and state levels, layered on top of broader demographic and economic pressures.

Population growth continues to support underlying demand for housing. Construction constraints continue to limit supply responsiveness in the short term. And private investors remain a significant source of rental housing across the country.

Within this context, Labor and the Coalition are operating with different policy instincts rather than fundamentally opposing goals. Both support increased supply, but differ on the balance between market incentives, government intervention, and taxation settings.

For investors, the key takeaway is that housing policy is no longer static. It is an active and evolving part of the investment environment — and one that can influence returns, risk, and strategy over time.

What was once a largely cyclical market driven by interest rates and construction activity is now also shaped by political direction.

And for anyone watching a weekend auction unfold, that political backdrop is becoming harder to ignore — even when no one on the footpath is talking about it.