The 2026-27 Federal Budget rewrote the rulebook for property investors — but it left one big door open. Here's why first-time buyers should be looking at new property instead of established stock.

If you've been saving for your first investment property and reading the news lately, you've probably noticed the mood has shifted. On 12 May 2026, Treasurer Jim Chalmers handed down a Budget that fundamentally changes how property investors are taxed — and from 1 July 2027, the playing field will look very different to the one your parents bought into.

The headline change is this: the long-standing 50 per cent Capital Gains Tax discount, which has let investors halve their tax bill when they sell, is being replaced for established property. In its place comes a new system that taxes "real" gains after inflation, with a minimum tax rate of 30 per cent. Negative Gearing on established residential property is also being pulled back.

There's one important exception. New builds — apartments, townhouses, duplexes and houses bought Off-the-Plan or built on vacant land — keep the old rules. That means for first-time investors, the maths now points clearly in one direction.

What actually changed

The Government's own tax reform page on Budget.gov.au confirms the headline change: it "will replace the 50 per cent Capital Gains Tax (CGT) discount with a discount based on inflation and introduce a minimum 30 per cent tax on gains from 1 July 2027."

In plain English, when you sell an investment property held longer than 12 months, you no longer get to halve your taxable gain. Instead, your purchase price is adjusted upward for inflation, and you pay tax on the "real" gain at your normal marginal rate — but never less than 30 per cent.

Negative Gearing — the rule that lets you offset rental losses against your wage income — is also being limited "to new builds from 1 July 2027, to focus tax support on new supply," according to Treasury. From 1 July 2027 onwards, an investor who buys established property after Budget night can still deduct losses, but only against income from other residential property — not against their salary.

There are two important transitional details for established property buyers. If you bought an established property before 7:30 pm on 12 May 2026, your Negative Gearing arrangements are fully grandfathered for the life of your ownership. For Capital Gains Tax, the position is more nuanced: any gain accrued before 1 July 2027 still gets the old 50 per cent discount, but the portion from 1 July 2027 onwards is taxed under the new rules. A market valuation at 30 June 2027 splits the cost base.

For new buyers of established property, neither concession survives in full.

Why Off-the-Plan is the loophole the Government left wide open

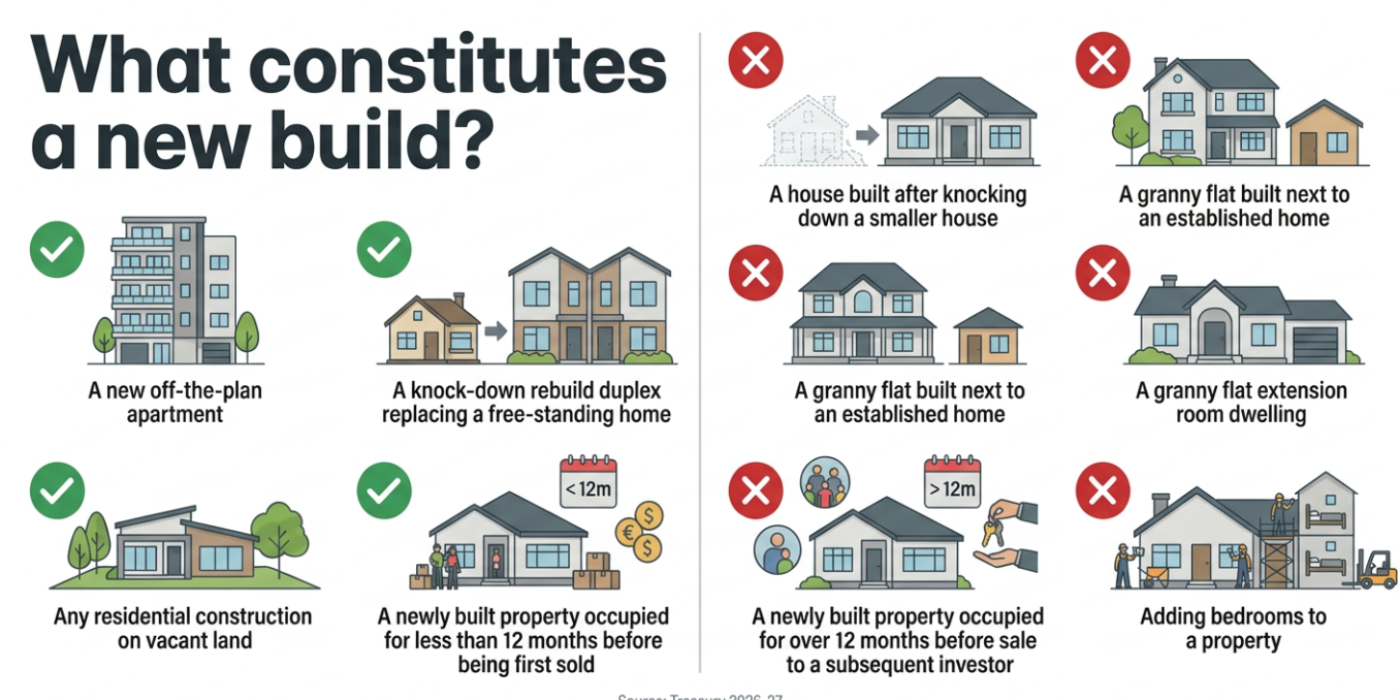

Treasury's stated goal is to push private investment toward new housing supply. To do that, the Budget carved out a generous exemption for "new builds" — and the definition is broad enough to drive a truck through.

The Budget papers spell out exactly what counts and what doesn't:

For these properties, two big concessions stay on the table. Negative Gearing still works the old way — rental losses can still reduce the tax on your wage. And when it comes time to sell, the Budget gives new-build investors a choice: as Treasury puts it, "Investors in new builds will be able to choose the 50 per cent CGT discount or the new arrangements."

That choice is the quiet superpower. Established-property investors get one tax treatment, and it's the less favourable one. New-property investors get to pick whichever method leaves them with less tax.

Side-by-side: established property vs Off-the-Plan

Imagine two first-time investors with identical circumstances. Both buy a $700,000 property, hold for ten years, and sell for $1.2 million. Inflation runs at about 2.3 per cent a year over the decade. Both earn around $100,000, which puts them in the 32 per cent marginal tax bracket including Medicare. The only difference is what they bought.

Capital Gains Tax comparison

Established property vs Off-the-Plan

$700,000 purchase · 10-year hold · sold for $1.2 million · 32% marginal tax rate

Established property

Post Jul 2027Off-the-Plan / new build

New buildIllustrative scenario based on the 2026-27 Federal Budget reforms taking effect 1 July 2027. Assumes 25% cumulative CPI over the hold and a 32% marginal tax rate (including Medicare). Your outcome will depend on your income, hold period, inflation and property performance. General information only, not personal tax or financial advice.

Sources

- Budget 2026-27 — Tax reform Treasury page confirming the 50% Capital Gains Tax discount replacement, the 30% minimum tax, and the new-build exemption

- Tax explainer — Negative Gearing and Capital Gains Tax Reform (PDF) Official 8-page factsheet from budget.gov.au

- Budget 2026-27 Overview (PDF) Treasury's 64-page overview document

- Budget Paper No. 2 — Budget Measures 2026-27 (PDF) Contains the new-build definition table and the "Boosting Home Ownership" measure

The new-property investor walks away with roughly $24,000 more after tax — before counting the years of Negative Gearing benefits that pile up along the way. The exact saving will shift with your income, the inflation rate during your hold, and how the property performs. But the structural advantage is real and built into the law.

Beyond the Capital Gains Tax discount

The tax change is the biggest reason to look at new property, but it's not the only one. State governments have their own incentives that stack on top.

In New South Wales, eligible Off-the-Plan buyers can defer stamp duty for up to 12 months, which frees up cash during construction. In Victoria, Off-the-Plan purchases let you pay stamp duty on the land value only, not the finished property — often a saving of tens of thousands of dollars on a typical purchase.

There are also practical advantages a beginner shouldn't dismiss. You lock in today's price for a property that won't settle for one to three years, giving any market growth in that period to you rather than the developer. The deposit is usually only 10 per cent, with the balance not due until settlement, so your savings keep earning interest. Building defects are covered by statutory warranties in every state. And the depreciation deductions on a brand-new property are far higher than on established property — another tax win that runs for years.

What to watch out for

Off-the-Plan is not risk-free. Construction delays are common, settlement valuations can come in below your contract price (called a "valuation shortfall"), and developer financial distress, while rare, can leave deposits at risk in extreme cases.

Three things matter most for a first-time buyer. Check the developer's track record — look for a solid history of completed projects with happy owners. Choose your location with rental demand in mind, not just price. And get your finance pre-approved before you sign, then keep your borrowing capacity strong all the way through to settlement.

The bottom line

If you'd bought an established investment property a year ago, you'd be sitting on the same generous tax concessions investors have enjoyed for 25 years. From 1 July 2027, those concessions are gone for new buyers of established property — but they live on for anyone who buys new property.

For a first-time investor, that asymmetry is hard to ignore. The Government has effectively put a "buy here" sign over the new-property market, and the tax math will reward those who read it.

This article is general information only and not personal tax or financial advice. Speak to a licensed accountant or financial adviser about your circumstances before deciding.

Sources

Budget 2026-27 — Tax reform: https://budget.gov.au/content/04-tax-reform.htm

Tax explainer — Negative Gearing and Capital Gains Tax Reform (PDF): https://budget.gov.au/content/factsheets/download/tax-explainers-negative-gearing-capital-gains-tax.pdf

Budget 2026-27 Overview (PDF): https://budget.gov.au/overview/download/budget-overview-2026-27.pdf

Budget Paper No. 2 — Budget Measures 2026-27 (PDF): https://budget.gov.au/download/bp2_2026-27.pdf